Find your degree

Let’s be real – unless your family is very wealthy, no one can truly save enough to cover all of your college expenses. College tuition rates are higher than they’ve ever been – and they’ve been going up 12% every year since 2010. But with good planning, you can make the most of your college savings with good choices, from scholarships and grants to work-study and other money hacks. Read on to find out how to maximize your college savings.

Disclaimer: Online College Plan does not provide financial guidance. This Student and Parent Savings Guide is for informational purposes only and should not be considered financial advice. All data and statistics were current at time of publication.

College Savings Tips and Tricks

Beginning to save for college as early as possible is crucial because it gives your money more time to grow. Even small contributions made regularly over time can accumulate significantly by the time your child is ready for college. Encourage your child to start saving early by opening a savings account or investment account specifically for college savings. Consider options like a custodial savings account, where your child can contribute money earned from part-time jobs, birthday gifts, or allowances. By instilling the habit of saving from a young age, you can maximize your education fund.

In 2022:

- 56% of parents said they were saving for their kids’ college

- One-third of families used a 529 or similar savings plans

- The average family had $18k in college savings

- The average family’s savings could cover 10% of college costs

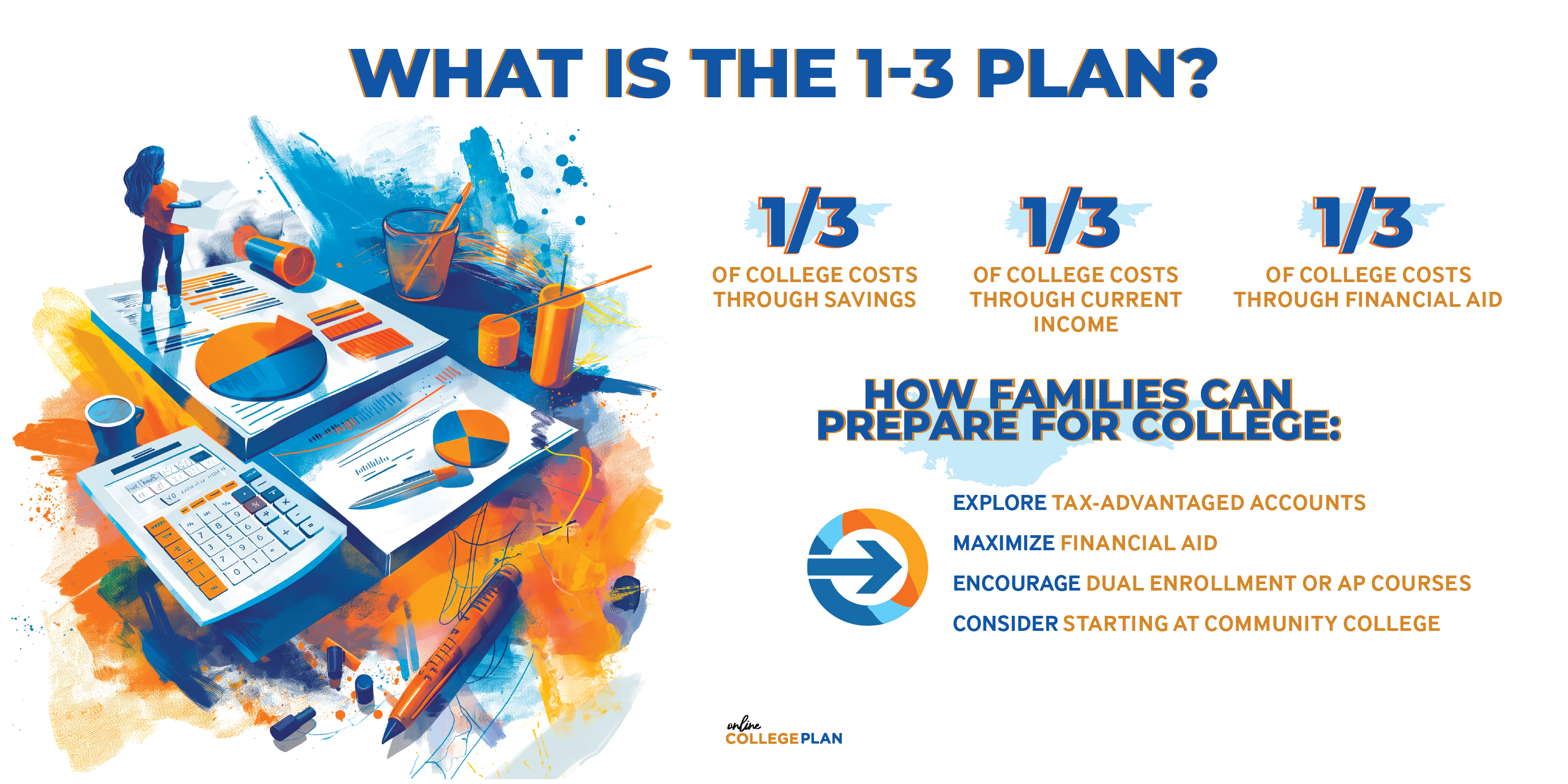

Explore Tax-Advantaged Accounts

Tax-advantaged college savings accounts, such as 529 plans and Coverdell Education Savings Accounts (ESAs), offer valuable benefits that can help you save more efficiently for college expenses. Contributions to these accounts grow tax-free, and withdrawals used for qualified education expenses are also tax-free. Additionally, many states offer tax incentives for residents who contribute to their state’s 529 plan. Take the time to research and compare the features of different accounts to determine which one best suits your needs and goals. By taking advantage of these tax-advantaged accounts, you can maximize your college savings and potentially reduce your tax burden at the same time.

Maximize Financial Aid

Financial aid can significantly reduce the cost of college, so it’s essential to research and apply for all available opportunities. This includes scholarships, grants, and work-study programs. Start by completing the Free Application for Federal Student Aid (FAFSA) to determine your eligibility for federal financial aid programs. Additionally, explore scholarship databases, both locally and nationally, to identify potential sources of free money for college. Be proactive in seeking out opportunities and submitting applications, as many scholarships have early deadlines. By maximizing your financial aid package, you can help offset the cost of college and reduce the need for student loans.

Encourage Dual Enrollment or AP Courses

Dual enrollment and Advanced Placement (AP) courses offer students the opportunity to earn college credits while still in high school, often at a reduced cost. By taking advantage of these programs, students can accelerate their path to degree completion and save money on tuition expenses.

Encourage your child to explore dual enrollment or AP course options that align with their academic interests and career goals. Contact your local community college to learn about dual enrollment options. Not only can these programs help students save money on college tuition, but they also provide valuable academic experiences that can strengthen college applications and prepare students for success in higher education.

Consider Starting at Community College

Starting at a community college can be a cost-effective way to earn college credits while keeping expenses low. Community colleges typically offer lower tuition rates compared to four-year universities, making them an affordable option for many students.

By completing general education requirements and prerequisite courses at a community college, students can save money on tuition expenses and transfer credits to a four-year institution later on. Additionally, many community colleges have transfer agreements with four-year universities, ensuring a smooth transition and maximizing the transferability of credits.

Starting at a community college allows students to explore different academic interests and career pathways without committing to a specific major or university right away. This approach can help students save money, gain valuable academic experience, and make informed decisions about their future education and career goals.

Exploring Scholarship and Grant Opportunities for College Savings

Securing scholarships and grants stands out as a top-notch strategy to lighten the financial load of college. Unlike loans, these financial aids don’t saddle you with debt, making them invaluable resources. Here’s a closer look at how you can enhance your chances of snagging these financial boosts:

- Start Early: The early bird gets the worm! Kickstart your scholarship hunt as soon as possible. Many scholarships come with early application deadlines, so procrastination could cost you valuable opportunities. By starting early, you give yourself ample time to research, prepare, and submit your applications without feeling rushed or overwhelmed.

- Cast a Wide Net: Don’t limit yourself to a narrow pool of scholarships. Cast your net far and wide by exploring various sources of financial aid. Look beyond your immediate surroundings and delve into local organizations, national foundations, corporate sponsors, and college-specific awards. Each source presents unique opportunities that could help fund your college journey.

- Tailor Your Applications: One size does not fit all when it comes to scholarship applications. Take the time to tailor each application to match the specific requirements and criteria of the scholarship. Highlight your achievements, extracurricular activities, community involvement, and unique experiences that demonstrate your eligibility and suitability for the award. Personalizing your applications increases your chances of standing out among the competition.

- Stay Organized: With multiple scholarship applications in the pipeline, staying organized is key to avoiding missed opportunities and deadlines. Create a system to track important dates, application requirements, and submission materials. Use spreadsheets, calendars, or dedicated apps to keep everything in order. Set reminders for deadlines and prioritize tasks to ensure you submit polished, on-time applications.

By adopting these strategies, you can navigate the competitive landscape of scholarship and grant opportunities with confidence and increase your chances of securing valuable financial aid for your college education.

Comparing Financial Aid Packages for College Savings

When weighing your college options, it’s crucial to carefully assess the financial aid packages offered to determine which choice makes the most financial sense. Here’s a detailed breakdown of the key factors to consider.

Grants and Scholarships

Take a close look at the amount of free money included in each financial aid package through grants and scholarships. Unlike loans, grants and scholarships do not require repayment, making them a valuable resource for reducing college expenses. Pay attention to both the quantity and quality of the awards offered, as higher amounts and renewable scholarships can significantly impact your overall financial outlook.

Loans

Delve into the details of the loans included in each financial aid package, including federal subsidized and unsubsidized loans, as well as private loans. While loans can provide immediate financial assistance, it’s essential to weigh the long-term implications of borrowing. Consider factors such as interest rates, repayment terms, grace periods, and potential future financial burdens. Aim to minimize reliance on loans and prioritize scholarships, grants, and work-study opportunities whenever possible.

Work-Study Opportunities

Investigate whether each college offers work-study programs, which allow students to earn money while gaining valuable work experience. Work-study opportunities not only provide financial support but also offer practical skills and networking opportunities that can enhance your academic and professional growth. Consider the availability of on-campus and off-campus work-study positions, as well as the flexibility of work hours to accommodate your academic schedule.

Overall Cost

Calculate the total cost of attendance for each college, taking into account tuition, fees, room and board, textbooks, transportation, and other miscellaneous expenses. Use college cost calculators and financial aid award letters to estimate your out-of-pocket expenses after accounting for grants, scholarships, and loans. Compare the net costs of attending each college to determine which option offers the most financial value. Keep in mind that the cheapest option may not always be the best fit academically or personally, so weigh all factors carefully before making a decision.

By carefully evaluating these factors, you can make informed decisions about which college offers the most cost-effective and financially sustainable choice for your higher education journey.

Budgeting for Textbooks and Other Expenses for College Savings

Textbooks and other expenses can quickly eat into your college savings, but with careful budgeting and smart spending, you can minimize costs and make your funds go further.

When I was a college student, I was able to use scholarship money to purchase books. However, some college bookstores no longer allow that, and some scholarships are only to be used for tuition.

Textbooks are a significant expense for many college students, but there are ways to save money without sacrificing academic quality. Consider:

- purchasing used or digital editions of textbooks

- renting books for the semester

- utilizing resources available at your campus library

Additionally, explore the option of sharing textbooks with classmates to further reduce costs and lighten the financial burden for everyone involved.

When it comes to other expenses, there are numerous opportunities to save money and stretch your college savings.

For instance, many colleges try to limit the number of cars on campus by making parking extremely expensive. If you live off-campus, carpooling with classmates or utilizing public transportation can help you save on parking transportation costs.

Managing textbook and surprise expenses wisely is essential for college students looking to make the most of their college savings. By prioritizing needs over wants, shopping smart for textbooks, and cutting costs where possible, you can minimize expenses and stretch your funds further. With careful budgeting and strategic planning, you can create a budget that works for you and helps you achieve your college savings goals.

What if I Just Pirate My Textbooks?

In the digital age, textbook piracy offers an easy way to save. Textbooks present a financial burden for a lot of students, and frankly, college bookstores are often predatory – no discounts, paying a fraction of the cost when they buy back your used books, and marking up used books.

The ethics of textbook piracy are a bit tricky. Some people say it’s a way to fight back against high textbook prices and unfair practices by bookstores. They argue that students should have easier and cheaper access to the materials they need for school. But there are concerns, too.

Pirating textbooks might seem like a smart way to save money, especially for students feeling the pinch. However, it can have consequences. It might not hurt the book publishers – big corporations that they are – but the people who wrote the books lose out on royalties and the motivation to write more books. Plus, there could be trouble at school if you’re caught. Some schools consider breaking copyright laws a student conduct issue.

Some college professors take a “look the other way” approach to textbook piracy. When I was a professor, I openly told my students I didn’t care how they got the books for my class. I even told them the campus bookstore was overpriced and to order used books online.

But it’s important to talk openly about the pros and cons. By having these conversations, we can work towards fairer solutions for everyone involved in education.

By implementing these college savings strategies, high school juniors and seniors, as well as current college students and their parents, can effectively manage the financial aspects of higher education. Remember to stay proactive, resourceful, and flexible in your approach to maximizing your education fund. With careful planning and perseverance, you can achieve your academic goals without undue financial stress.

FAQs

The best savings plan for college depends on your individual circumstances and financial goals. However, popular options include 529 college savings plans and Coverdell Education Savings Accounts (ESAs). Both offer tax advantages and flexibility in saving for future education expenses. It’s essential to research and compare different plans to find the one that best suits your financial planning for college.

The 1-3- rule for college savings suggests that families should aim to cover:

• one-third of college costs through savings

• one-third through current income

• one-third through financial aid

This guideline helps families balance their college savings efforts with other financial priorities and sources of funding. It may not be manageable for all families, but it is just a way of thinking about college savings.

The 529 savings strategy involves utilizing a 529 college savings plan to save for education expenses. This tax-advantaged investment account allows contributions to grow tax-free and can be used to cover qualified education expenses such as tuition, fees, books, and room and board. Families can choose from a variety of investment options and may be eligible for state tax benefits, making 529 plans a popular choice for college savings.

The quickest way to save for college is to start early and save aggressively. Maximize contributions to tax-advantaged accounts like 529 plans, consider high-yield savings accounts or investment vehicles with potential for growth, and look for opportunities to cut expenses and increase savings. Additionally, explore scholarships, grants, and other financial aid options to supplement your savings efforts and reduce the overall cost of college.

Yes, 529 plans are often worth it for many families saving for college. These plans offer several benefits, including tax advantages such as tax-free growth and tax-free withdrawals for qualified education expenses. Additionally, many states offer additional tax incentives for residents who contribute to their state’s 529 plan. Furthermore, 529 plans typically offer flexibility in terms of investment options and contribution amounts, making them a versatile tool for college savings. However, it’s essential to carefully consider your individual financial situation and goals before deciding if a 529 plan is the right choice for you.

However, 529 plans have some potential downsides to consider:

• Limited Investment Options: Although 529 plans typically offer a range of investment options, they may be more limited compared to other investment vehicles. This lack of flexibility could impact your ability to tailor your investment strategy to your specific needs and preferences.

• Penalties for Non-Qualified Withdrawals: If you withdraw funds from a 529 plan for non-qualified expenses, you may be subject to income tax on the earnings portion of the withdrawal, as well as a 10% penalty. This penalty could significantly reduce the value of your savings if you use the funds for purposes other than education.

• Impact on Financial Aid Eligibility: Funds held in a parent-owned 529 plan are typically treated as parental assets for financial aid purposes, which can have a moderate impact on eligibility for need-based financial aid. However, distributions from the plan to pay for qualified education expenses are not counted as income on the Free Application for Federal Student Aid (FAFSA).

• State-Specific Considerations: Each state’s 529 plan may have unique features, benefits, and fees. It’s essential to research and compare plans carefully to ensure you select the one that best fits your needs and goals.

• Market Risk: Like any investment, 529 plans are subject to market risk, and the value of your investments may fluctuate over time. While most plans offer age-based investment options that automatically adjust asset allocation based on the beneficiary’s age, there is still inherent risk involved.

Overall, while 529 plans offer significant advantages for college savings, it’s essential to weigh these potential downsides against the benefits and consider your individual circumstances before making a decision. Consulting with a financial advisor can help you make an informed choice.